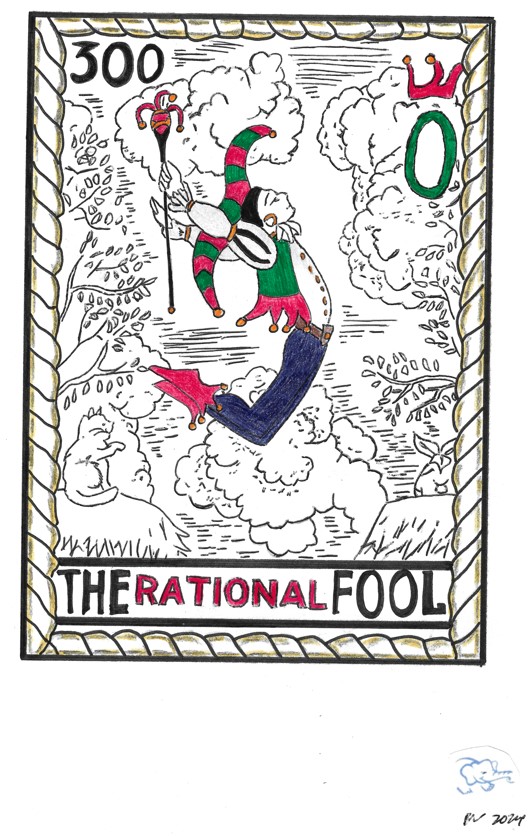

"People who always give nothing are rational fools who blindly follow material self-interest." --- Richard Thaler (2016)

Inspired by Richard Thaler’s Misbehaving: The Making of Behavioral Economics, the “Rational Fool” serves as a whimsical yet thought-provoking representation of the human tendency to act against our own best interests despite possessing rational capabilities. This concept, rooted in behavioral economics, challenges the traditional economic assumption of humans as perfectly rational decision-makers.

This drawing aims to spark curiosity and discussion around the fascinating intersection of psychology and economics, highlighting the importance of understanding behavioral biases in our everyday lives.

Through this playful visual metaphor, I invite visitors to explore the intriguing complexities of human behavior and decision-making, ultimately encouraging a deeper appreciation for the nuances of our choices.

Downloadable Content – Raw Notes

Interested in diving deeper into Richard Thaler’s work on Misbehaving? Download my unfiltered notes below 👇

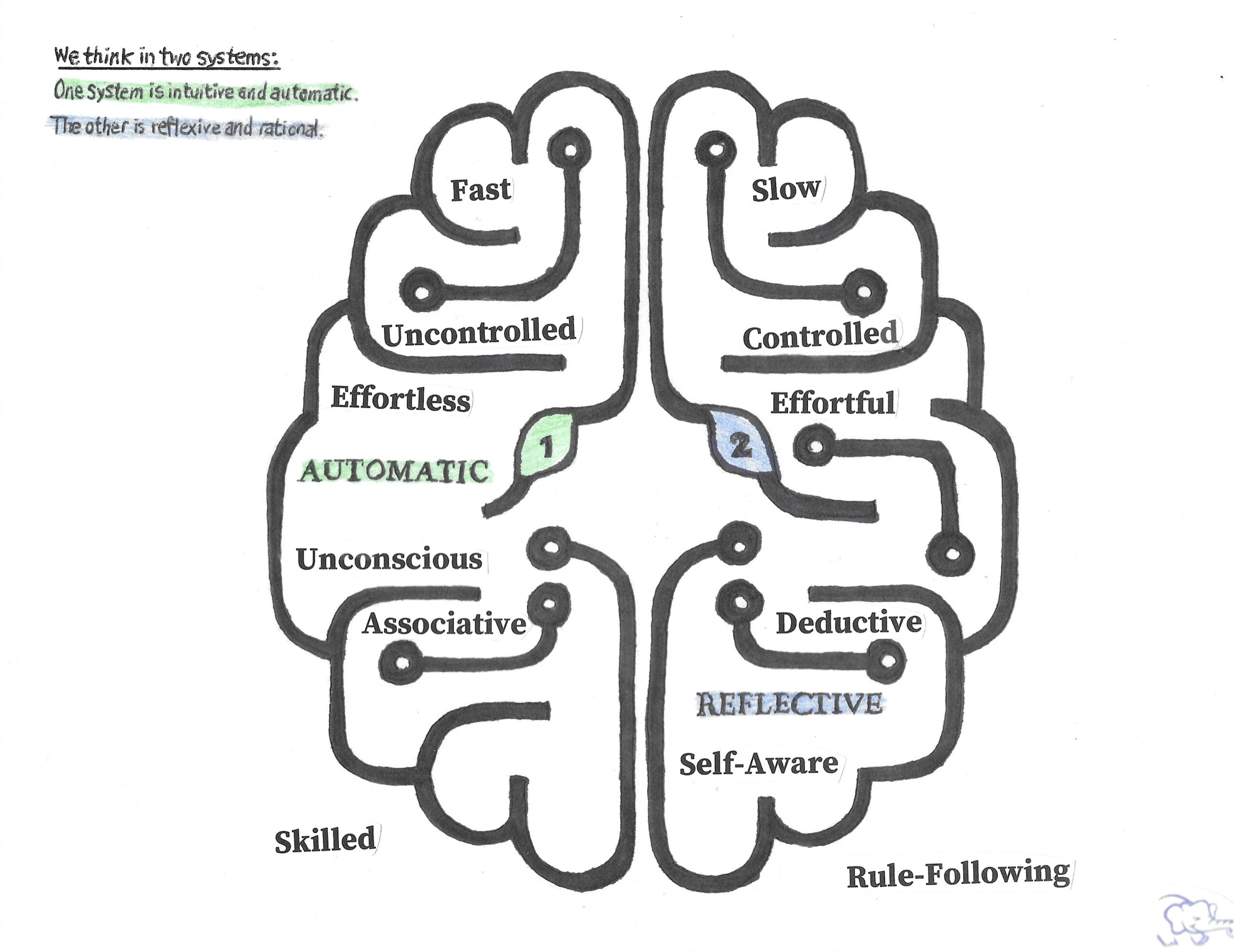

“There are two systems of thought: The Intuitive System 1, which does the fast thinking, and the effortful and slower System 2 which does the slow thinking, monitors System 1, and maintains control as best it can within its limited resources.”

--- Daniel Kahneman, Thinking Fast and Slow (2011)

Introduction

The fact remains whether we like to admit it or not, our minds are susceptible to systematic errors in thinking and judgment. And when we are under pressure or lacking total information, our minds are strongly biased toward causal explanations. To wrap our minds around all the ways we make mistakes in our thinking and judgment, Daniel Kahneman simplified the mind into two systems:

The Intuitive System 1 thinks VERY FAST

The effortful and controlled System 2 thinks VERY SLOWLY

The point Kahneman drives home in his book is by learning to recognize these patterns of thinking in yourself, you can minimize the mistakes when the stakes are highest.

System One … The Hare … All Gas No Brakes!

To put it quite simply: System 1 thinking is impulsive and intuitive and is designed to jump to conclusions from very little evidence. What’s worse, System 1 isn’t designed to know the size of the jumps it is making in its thinking. With System 1, WHAT YOU SEE IS ALL THERE IS (WYSIATI), and because of this, only the evidence at hand counts. In the absence of an explicit context, System 1 will generate its own context, and it really excels at constructing the best possible story … Are you scared yet? If not you should be!

System 1 is highly adept in one form of thinking … Automatic and Effortless. It identifies causal connections between events, sometimes even when the connection itself is spurious.

System Two … The Tortoise … All Brakes No Gas!

Like most things in life, there is a yin-and-yang or balance to things. Your brain’s method of thinking is no different. If System 1 is your default, fast, and reflexive method of thinking, System 2 is the opposite of this. To be specific, System 2 controls thoughts and behaviors, and it is the only system that can follow rules, compare objects on several attributes, and make deliberate choices between options.

Okay… Now What?

Here is the thing… Regardless of Systems 1 and 2, our brains are pattern-matching machines subject to a plethora of cognitive biases. Here are a couple of my favorites:

Anchoring Effect

Availability Heuristic

Halo Effect

Hindsight Bias

Representativeness Heuristic

We often ignore relevant statistical facts and we rely almost exclusively on rules of thumb. When you factor in that System 1 is our default fast way of thinking, and the deep, deliberate, and controlled System 2 way of thinking is lazy and hard to consistently deploy, it’s not surprising that we humans make a ton of decision-making errors. Often, we are inconsistent in our evaluations, and we often make errors in summary judgments. Kahneman found in his research that humans when asked to evaluate the same information twice frequently give different answers.

Reading through Daniel Kahneman’s work convinces me of a couple of solutions to human decision-making shortcomings that a lot of us humans are not going to like to hear… Humans need help to make good decisions, and there are informed and unobtrusive ways to provide this help:

Whenever we can replace human judgment with a formula, we should at least consider it.

Since machines are more likely than human judges to detect weakly valid cues, we should consider complementing or augmenting human-only judgments with human + machine judgments

Maximize predictive accuracy by using machine logic, especially in low-validity environments

Conclusion and Final Thoughts

In Thinking Fast and Slow, Daniel Kahneman set out to improve the ability in all of us to identify and understand errors of judgment, and choice in others, and ultimately in ourselves! He wanted to provide his readers with a richer and more precise language to discuss decision-making and thinking within the brain. Because our System 1 method of thinking is our default and intuitive way of thinking, it’s easy for us to ignore relevant statistical facts that don’t fit the patterns we want. By nature, our slower and more methodical way of thinking (System 2) takes more time than we want and is lazy by nature. Humans need help to make good decisions because there is overwhelming evidence that we Humans can’t think rationally 100% of the time.

What Will I Do Differently As a Result of This Book?

Learn to recognize situations in which mistakes are likely and try harder to avoid making significant decision-making mistakes when the stakes are high

Understand that even when I think that I am being rational there is a good chance my default System 1 way of thinking has quickly pattern-matched and downplayed disconfirming information.

Understand how deep the halo effect goes in clouding/painting my judgment of a person with a favorable first impression versus not.

The major source of error in forecasting is our prevalent tendency to underweight or ignore distributional information. We forecast based on information in front of us (WYSIATI).

Consequently, I will therefore make every effort to frame the forecasting problem so as to facilitate utilizing all the distributional information that is available

Here is the thing … We are pattern seekers, believers in a coherent world in which regularities appear not by accident but as a result of mechanical causality or of someone’s intention.

This fact means that we humans often misclassify random events as systematic and we are far too willing to reject the belief that much of what we see in life is random.

This means for me, as I continue to plan I MUST EMBRACE THE RANDOMNESS OF LIFE!

Lastly, beware when I am in a good mood and I have had limited sleep … My System 2 will be weaker than usual and I should pay extra attention to my default System 1.

Downloadable Content

Thinking Fast, and Slow is a must-read for anyone interested in gaining insights into the Human mind and the manner in which decisions are made. The following book notes have been created to help you with your understanding of Daniel Kahneman’s concepts within Thinking Fast, and Slow.

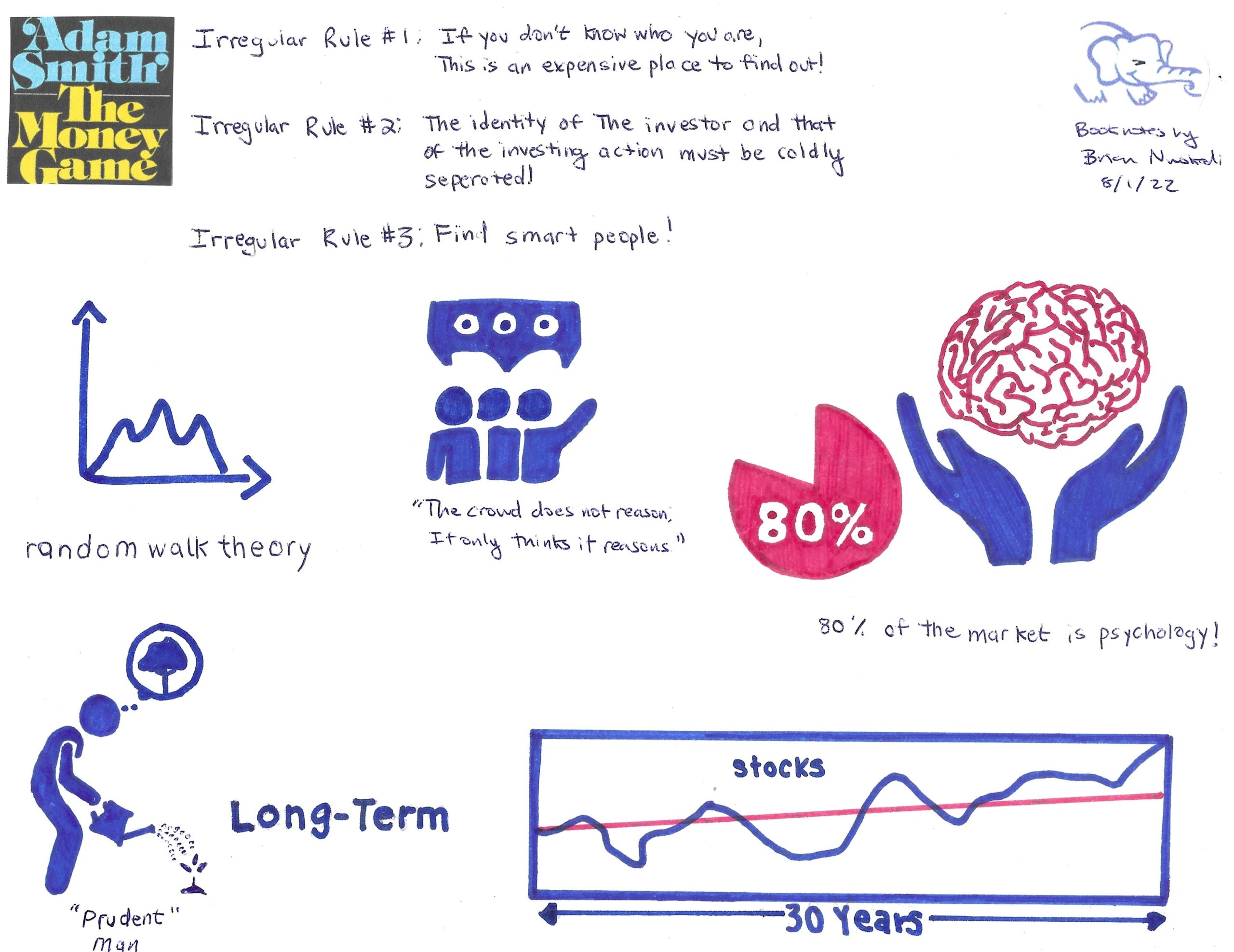

What if I told you that the whole point of the stock market is not to make money? What if I told you that the stock market itself is just a Game, and the real object of this Game is not money; it’s the playing of the Game itself?

In The Money Game Adam Smith (also known as George J. W. Goodman) sets out to explain how the stock market is a Game to be played with objectives that oftentimes do not make sense. While money preoccupies so much of our consciousness, The Money Game is adamant that making money is not the real objective of playing the stock market Game. The sooner we realize that the stock market Game is an irrational one, the better we will play it.

Through a series of chapters asking questions and describing real events and real characters (real but masked), George J. W. Goodman sets out to explore the unexplored area of the markets … the emotional area. As he states very eloquently in Chapter 2, “There are fundamentals in the marketplace, but the unexplored area is the emotional area. All charts and breadth indicators and technical palaver are the statistician’s attempts to describe an emotional state.

In the end, the one requirement to win The Money Game is to remember the Irregular Rule: If you don’t know who you are, this is an expensive place to find out. Emotional maturity must be displayed over the long run if you are going to survive the game called the stock market.

My Summary Conclusions from Each Chapter

Part I. YOU: Identity, Anxiety, Money: Chapter 1-9

Preface: The game we create with it is an irrational one, and we play it better when we realize that, even as we try to bring rationality to it.

• Chapter 1: The word game was deliberately chosen to describe the stock market and the sooner that all of us small investors understand that this is a game, the better off we may be.

• Chapter 2: Do not forget the Irregular Rule: If you don’t know who you are, this is an expensive place to find out!

• Chapter 3: It all comes back to the Irregular Rule that you must know yourself for the stock market is an expensive place to find that out. The requirement to win this game is emotional maturity.

• Chapter 4: Since 80% of the market is psychology or deeper still human emotionality, the market can really be seen as a crowd. Because of this tendency, there is no substitute for good information, good research, and good ideas.

• Chapter 5: On one hand you have Adam Smith the father of modern economics stating definitely that money is about the maximization of profit and in some sense the accumulation of wealth (i,e. The Wealth of Nations). On the other hand, you have Norman Brown who sees money as a noose around our necks that ultimately makes our human nature impoverished. You must decide for yourself!

• Chapter 6: There are countless reasons people get into the Game. Some people love to gamble and lose. Others just want to make money over the long term by owning stocks forever. Regardless of your reason, you need to know yourself and stick to your plans.

• Chapter 7: The only real protection against all the ups and downs of the market (the anxiety) is to have an identity so firm it is not influenced by all the brouhaha in the marketplace. And remember, the stock doesn’t know you own it!

• Chapter 8: So if we are talking about real big money, forget the stock market. Build a company and have the market capitalize on your earnings.

• Chapter 9: The “simple equation of wealth”: To get rich, you find a stock whose _ has been compounding at a very fat, and then the stock zooms, and there you are.

Part II. IT: Systems: Chapter 10-14

Chapter 10: Charting assumes that what was true yesterday will also be true tomorrow. But you and I know that past patterns/performance are not predictive of future patterns/performance.

• Chapter 11: To quote Professor Fama, “the history of the series of stock price changes cannot be used to predict the future in any meaningful way. The future path of the price level of security is no more predictable than the path of a series of cumulated random numbers. If the random walk is indeed Truth, then all charts and most investment advice have the value of zero, and that is going to affect the rules of the Game.

• Chapter 12: The Game is such that computers take away any long-term advantages individuals find. Our only chance is to rely on luck (random walk thesis).

• Chapter 13: The numbers created by “independent auditors” should be looked at with a grain of salt given that the accountants are paid and hired by the companies themselves.

• Chapter 14: Someone has to be on the losing end of the transaction and that is usually the little investor.

Part III. THEY: The Pros: Chapter 15-18

Chapter 15: Professional investors are “performance” managers who are focused on driving results in the short term. Very few “performance” managers think in the long term. It’s all about driving big capital gains!

• Chapter 16: Like everything in life, those that are really in the know!

• Chapter 17: The market does not follow logic, it follows some mysterious tide of mass psychology.

• Chapter 18: If you are in the right thing at the wrong time, you may be right but have a long wait; at least you are better off than coming late to the party.

Part IV. VISIONS OF THE APOCALYPSE: Can it All Come Tumbling Down? Chapter 19-20

Chapter 19: Sooner or later you have to come to reality, and stop being a father to the world. Lead it, yes. Buy it. No.

• Chapter 20: Sure, it can all come tumbling down. All it takes is for belief to go away!

Part V. VISIONS OF THE MILLENNIUM: Do You Really Want to Be Rich?

Chapter 21: You need to create your own money philosophy to answer the question do you really want to be rich?

Visual Summary of Key Findings from Book

“Unfortunately, as we have seen, the playing of the Game is not entirely a rational affair. There is nothing so disastrous, said Lord Keynes as a rational investment policy in an irrational world”

Having finished the 750+ page tome to Capital by Thomas Piketty well over a year ago, I have just gotten around to writing up what I learned. In attempting to summarize this book, I realize that there is no way I can cover everything I learned. Quite simply, Piketty has blown my mind with the depths of his research. This book is the deepest source I have ever read on how capital behaves and why wealth and income inequality are two sides of different coins.

I figure that the best approach with this write-up is to break it down into manageable chunks. What follows below is a summary of the theoretical characteristics of Capital and how it behaves in the world today as well as in the past. I’ll unpack the features of income, capital, and output and how each of these dynamics interplay with one another.

The next write-up at a later date yet to be determined, will delve into the impacts that Capital has had on inequality. I’ll unpack the structure of inequality and some potential solutions that Piketty mentions. This review is by no means a political or opinion piece. I am simply sharing some of the learnings I received from diving into this book.

With that, let’s dive in…

Is r > g the Central Contradiction of Capitalism?

The first concept that Piketty spends time unpacking is the relationship between returns on capital and the overall growth rate of the economy. Piketty boldly states that growth in the future will slow and capital will be that much more important. As economic growth slows and falls below the average rate of return on capital, past wealth naturally takes on a larger importance. This is simply because it takes only a small flow of new savings to increase the stock of wealth steadily.

Thomas Piketty’s First Fundamental Law of Capitalism

The second concept that Piketty spends time unpacking is what he calls his First Fundamental Law of Capitalism. This law shows how important capital is in relation to the national income of a country. As the nature of wealth over the long run continues to transform (i.e., capital used to be agricultural and has since been replaced by industrial, financial capital, and urban real estate), its importance as measured by the capital/income ratio has remained steady and unchanged.

Thomas Piketty’s Second Fundamental Law of Capitalism

The third concept that Piketty spends time unpacking is what he calls his Second Fundamental Law of Capitalism. This law shows that countries with high savings rates and low growth rates accumulate enormous stocks of capital relative to their incomes over the long run. This can have significant effects on the social structure and distribution of wealth in a country. Piketty emphasizes that the impacts of this law are gradual and take decades to manifest. Boldly, Piketty predicts that by 2100 the entire planet could look like Europe at the turn of the 20th century with a capital/income ratio of 6-7 years.

The Dynamics of the Capital/Income Ratio in Europe and the U.S.

By investigating the dynamics of the capital/income ratio of Britain, France, Germany, and the United States, Piketty uncovers that the nature of capital in these rich countries has changed: capital was once mainly land but has now primarily become housing, industrial, and financial assets. But capital’s importance remains the same.

The Dynamics of the Capital/Income Ratio in Britain

In Britain, private wealth in 2010 accounted for 99% of national wealth and the bulk of the pubic debt in practice was owned by a minority of the population. Britain in summary is a country with accumulated capital based on public debt and the reinforcement of private capital.

The Dynamics of the Capital/Income Ratio in France

In France, private wealth in 2010 accounted for 95% of national wealth and the bulk of wealth in France was driven by accumulations of significant public assets in the industrial and financial sectors followed by major waves of privatization of these same assets. In a sense, France is a country with a model of Capitalism without Capitalists.

The Dynamics of the Capital/Income Ratio in Germany

In Germany, capitalism takes on a more social ownership point of view. Prevalent in the German marketplace is the stakeholder model of business where firms are owned not only by shareholders but also by certain other interested parties like the firms’ workers themselves. This Rhenish Capitalism has resulted in lower stock market valuations for German firms when compared to British & French firms.

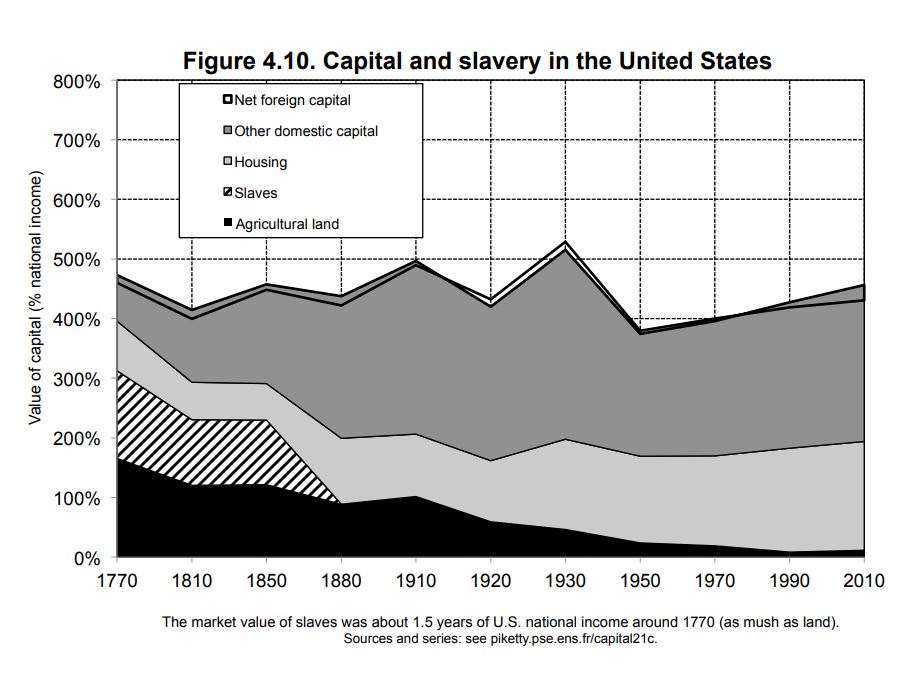

The Dynamics of the Capital/Income Ratio in the United States

In the United States, more than 95% of the assets are American-owned but the influence of landlords and historically accumulated wealth was less important in the U.S. than in Europe. However, the structure of capital in the United States took on a different form. Specifically in the South, slave capital largely supplanted and surpassed landed capital. So much so, that the total market value of slaves represented nearly a year and a half of U.S. national income in the late 18th and first half of the 19th century.

Conclusion

A market economy based on private property, if left to itself, contains power forces of divergence, which are potentially threatening to democratic societies and to the values of social justice on which they are based. My next write-up on Capital in the Twenty-First Century by Thomas Piketty will dive into the immense inequalities of wealth that have occurred as a result of the natural dynamics of capital.

Matt Groening was once said, “Donuts. Is there anything they can’t do?” And for Kate Raworth, doughnutsare rewriting everything you ever learned in Economics 101. Her book, Doughnut Economics, is a simple referendum on modern day economics. Her thesis is quite simple:

Leaders of 2050 are being taught an economic mindset that is rooted in the textbooks of 1950, which in turn are rooted in the theories of 1850.

This “archaic” economic mindset has led our current world astray, and thus a new way of thinking for the 21st Century is much needed.

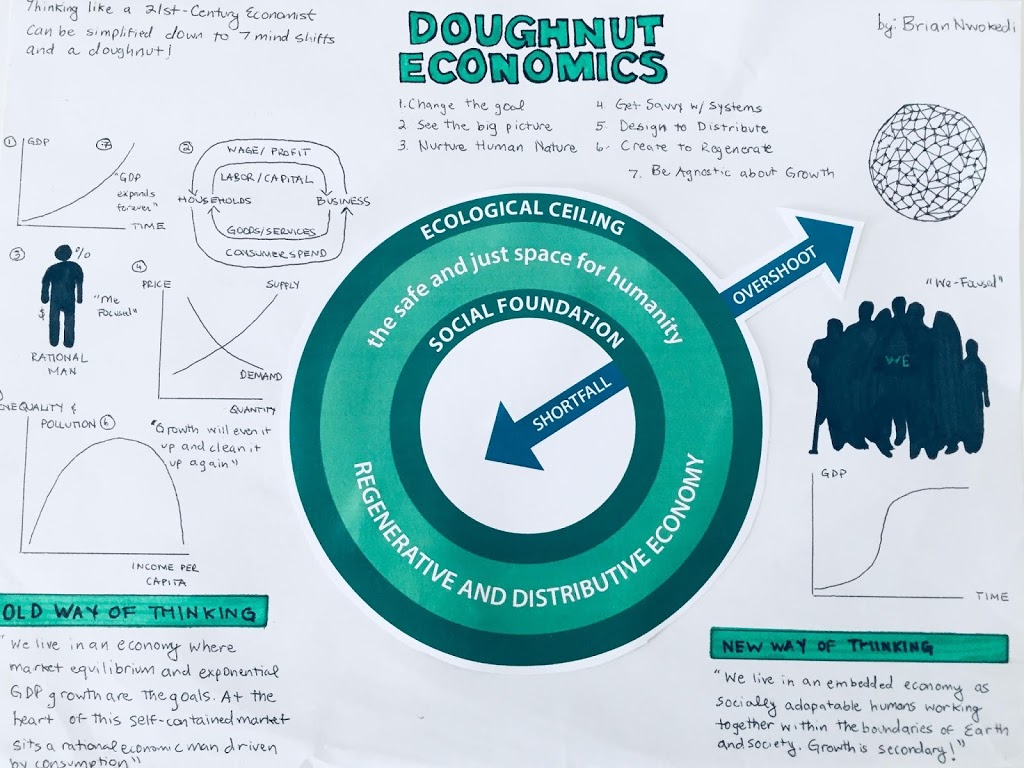

Enter the Doughnut

The essence of the doughnut is a social foundation of well-being that no one should fall below, and an ecological ceiling of planetary pressure that we should never go beyond. It is in between these two layers that lies a safe and just space for us all:

In order to remain within the boundaries of the doughnut, current economic thinkers and policy makers need to change their default modus operandi. Raworth identifies seven specific ways to change economic thinking and policy making for the better:

1.Change the Goal from GDP to the Doughnut

2.See the Big Picture from self-containing market to embedded economy

3.Nurture Human Nature from rational economic man to social adaptable humans

4.Get Savvy with Systems from mechanical equilibrium to dynamic complexity

5.Design to Distribute from ‘growth will even it up again’ to distributive by design

6.Create to Regenerate from ‘growth will clean it up again’ to regenerative by design

7.Be Agnostic about Growth from growth addicted to growth agnostic

The following picture is my visual representation of what Doughnut Economics represents to me.

Shifting from Conventional Economics to Doughnut Economics Will Help Planet Earth and All Humankind Thrive

The current economic pursuit of GDP first pushes every consumer in our global economy to spend money they don’t have on things they don’t really need (think consumerism 101). It’s an endless hamster wheel of more for the sake of more, and it requires continual growth in income and output to support it.

By changing the goal of our global economy from GDP to the Doughnut we ignore conventional economic theory that posits every citizen’s satisfaction or happiness is based on the consumption of more goods. And this switch in focus will allow us to better advance the richness of human life on earth.

Underlying the big shift in economic focus is another underlying shift in the characterization of humans and their nature. Conventional economic theory posits that humans are rational and make decisions that solely maximize their utility which equates to driving satisfaction through consumption.

But the reality of life for each of us is we are far from solitary figures. Instead, we are social adaptive beings that thrive best in environments where we can relate to each other. Thus, our global economic machine is best served by putting the collective “WE” at the focus instead of growth in “GDP” at the focus.

It’s Clear We Have an Economic Design Problem … The Question is Will We Fix It?

In the 21stcentury, we have transgressed at least four planetary boundaries and have created a global economy that has left billions of people still facing extreme deprivation. On top of that, the current global economy has allowed the richest 1% to own half of the world’s financial wealth.

At the heart of income and wealth inequality lies a simple design question: who owns the enterprise, and so captures the value that workers generate? Our current economic system is designed in such a way that shareholders own the enterprise and thus capture the value generated by workers as evidenced by the following:

From 2002 – 2012 worker productivity grew +30% while real wage growth remained practically non-existent. This trend was so dreadful that economists have dubbed this ten-year period the “Lost Decade for Wages.” Meanwhile, returns to shareholders grew faster than the economy as a whole.

Furthermore, it’s beyond clear now that our economic system is the actual root cause of the ecological crisis that we currently face as humankind on this Earth (see hereand here). At the heart of Earth’s ecological decline lies a simple design flaw in our current global economy:

We extract Earth’s minerals, metals, biomass, and fossil fuels and manufacture them into products. These products are eventually sold to consumers who use then but eventually throw them away. The very essence of this cradle-to-grave type industrial economic system is destructive to Earth’s ecological system.

Given the societal and ecological challenges we face, it’s up to us to decide whether or not we want to fix the economic design problem we have.

In Closing

In 2015, world GDP was $80 trillion. An expectation of 3% indefinite growth would mean that …

(1)By 2050 the world economy would be 3x bigger than 2015

(2)By 2100 the world economy would be 10x bigger than 2015

(3)By 2200 the world economy would be 240x bigger than 2015

It’s beyond clear that this expectation of indefinite growth can not be possible without destroying our Earth and society! Alarm bells should be going off in each and every one of us from citizens to politicians.

It’s time for us to accept the fact that we have reached the logical conclusion of our expansionist economic paradigm, and redesign a global economy that is focused on the promotion of human prosperity whether GDP is going up or down. This will be an extremely hard shift in paradigm, but it will be absolutely vital if we are going to make it as a planet and society for the next 100 years.