"Success with money relies more on Psychology than Finance,and doing well with money has little to do with how smart you are, and a lot to do with how you behave. And behavior is hard to teach, even to really smart people." --- Morgan Housel (2020)

📚 Core Insight

Success with money is about behavioral discipline, not technical intelligence.

Smart people fail financially because behavior > IQ when it comes to money.

Emotional control, patience, decision-making matter more than financial formulas.

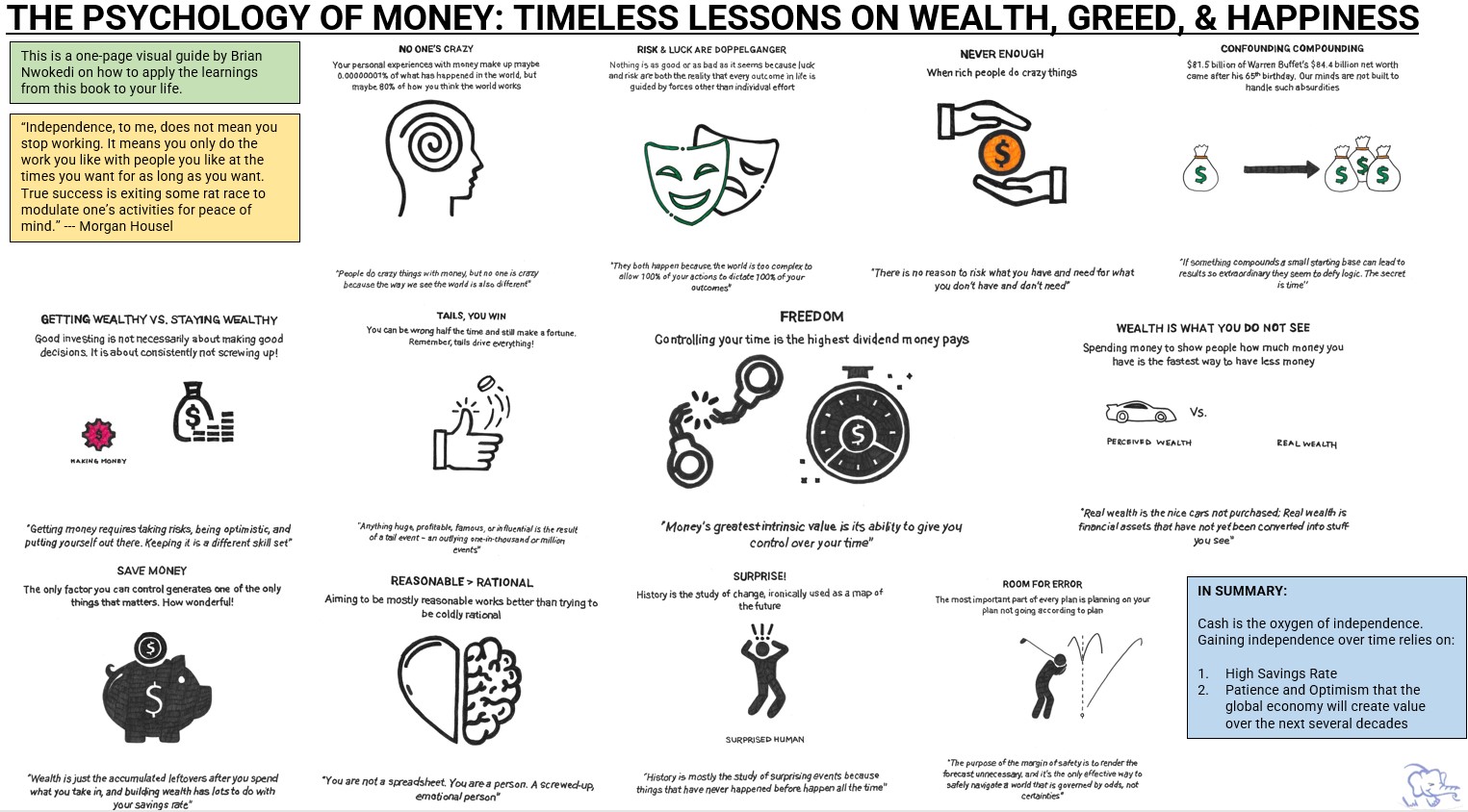

“The Psychology of Money“ by Morgan Housel is an insightful guide that puts the spotlight of financial success squarely on the shoulders of human behavior. In this world of complexity, how you behave with money is more important than what you know about money.

With a blend of research, anecdotes, and stories of personal experiences, Housel illuminates the significance of better understanding your own behavior, and how that is far more responsible for your financial outcomes than your skill.

The following one-page visual guide has been created by me to help you apply the teachings from Morgan’s book to your life. See below ?

Downloadable Content – Raw Notes

Ready to dive deeper into Morgan Housel’s work on The Psychology of Money? Download my unfiltered notes below ?

“However, I am confident in saying that if you can figure out a way to save 10% to 20% of your income into the financial markets each year, automate your savings and all of your bill payments, increase the amount you save each year by just a little, diversify your investments, and basically leave them alone, you will be better off financially than the vast majority of retirement savers in America. Everything else is gravy.” --- Ben Carlson(2020)

📚 Core Insight

Building financial independence isn’t about complex investment strategies — it’s about mastering simple behaviors consistently over decades.

The real drivers of retirement success are: saving early and often, automating your habits, resisting lifestyle inflation, and focusing relentlessly on what you can control (your savings rate and behavior) — not chasing high investment returns.

Patience, discipline, and consistency—not brilliance—win the long game.

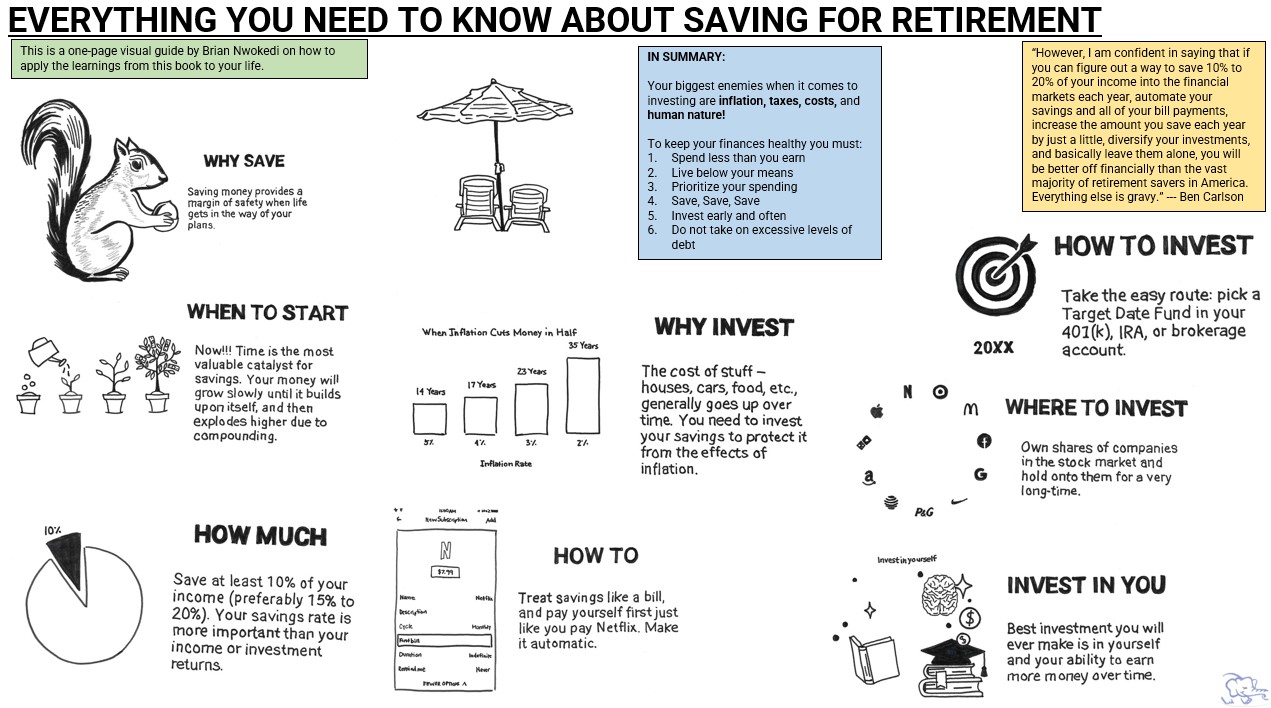

“Everything You Need to Know About Saving for Retirement“ by Ben Carlson is a succinct yet insightful guide that puts the spotlight on a fundamental aspect of retirement planning: your savings rate. In a world of complex investment strategies and ever-changing financial landscapes, Carlson distills his wisdom into a straightforward message – it’s not just about where you invest, but how much you save.

With a clear and approachable style, he emphasizes that building a secure retirement is within reach if you focus on increasing your savings and maintaining a consistent approach. Drawing on his expertise in personal finance, Carlson’s concise and no-nonsense approach empowers readers to take control of their financial destinies, offering a roadmap to achieving financial security during retirement through a smart savings strategy!

The following one-page visual guide has been created by me to help you apply the teachings from Ben’s book to your life. See below ?

Downloadable Content – Raw Notes

Ready to dive deeper into Ben Carlson’s work on Saving for Retirement? Download my unfiltered notes below ?

Having finished the 750+ page tome to Capital by Thomas Piketty well over a year ago, I have just gotten around to writing up what I learned. In attempting to summarize this book, I realize that there is no way I can cover everything I learned. Quite simply, Piketty has blown my mind with the depths of his research. This book is the deepest source I have ever read on how capital behaves and why wealth and income inequality are two sides of different coins.

I figure that the best approach with this write-up is to break it down into manageable chunks. What follows below is a summary of the theoretical characteristics of Capital and how it behaves in the world today as well as in the past. I’ll unpack the features of income, capital, and output and how each of these dynamics interplay with one another.

The next write-up at a later date yet to be determined, will delve into the impacts that Capital has had on inequality. I’ll unpack the structure of inequality and some potential solutions that Piketty mentions. This review is by no means a political or opinion piece. I am simply sharing some of the learnings I received from diving into this book.

With that, let’s dive in…

Is r > g the Central Contradiction of Capitalism?

The first concept that Piketty spends time unpacking is the relationship between returns on capital and the overall growth rate of the economy. Piketty boldly states that growth in the future will slow and capital will be that much more important. As economic growth slows and falls below the average rate of return on capital, past wealth naturally takes on a larger importance. This is simply because it takes only a small flow of new savings to increase the stock of wealth steadily.

Thomas Piketty’s First Fundamental Law of Capitalism

The second concept that Piketty spends time unpacking is what he calls his First Fundamental Law of Capitalism. This law shows how important capital is in relation to the national income of a country. As the nature of wealth over the long run continues to transform (i.e., capital used to be agricultural and has since been replaced by industrial, financial capital, and urban real estate), its importance as measured by the capital/income ratio has remained steady and unchanged.

Thomas Piketty’s Second Fundamental Law of Capitalism

The third concept that Piketty spends time unpacking is what he calls his Second Fundamental Law of Capitalism. This law shows that countries with high savings rates and low growth rates accumulate enormous stocks of capital relative to their incomes over the long run. This can have significant effects on the social structure and distribution of wealth in a country. Piketty emphasizes that the impacts of this law are gradual and take decades to manifest. Boldly, Piketty predicts that by 2100 the entire planet could look like Europe at the turn of the 20th century with a capital/income ratio of 6-7 years.

The Dynamics of the Capital/Income Ratio in Europe and the U.S.

By investigating the dynamics of the capital/income ratio of Britain, France, Germany, and the United States, Piketty uncovers that the nature of capital in these rich countries has changed: capital was once mainly land but has now primarily become housing, industrial, and financial assets. But capital’s importance remains the same.

The Dynamics of the Capital/Income Ratio in Britain

In Britain, private wealth in 2010 accounted for 99% of national wealth and the bulk of the pubic debt in practice was owned by a minority of the population. Britain in summary is a country with accumulated capital based on public debt and the reinforcement of private capital.

The Dynamics of the Capital/Income Ratio in France

In France, private wealth in 2010 accounted for 95% of national wealth and the bulk of wealth in France was driven by accumulations of significant public assets in the industrial and financial sectors followed by major waves of privatization of these same assets. In a sense, France is a country with a model of Capitalism without Capitalists.

The Dynamics of the Capital/Income Ratio in Germany

In Germany, capitalism takes on a more social ownership point of view. Prevalent in the German marketplace is the stakeholder model of business where firms are owned not only by shareholders but also by certain other interested parties like the firms’ workers themselves. This Rhenish Capitalism has resulted in lower stock market valuations for German firms when compared to British & French firms.

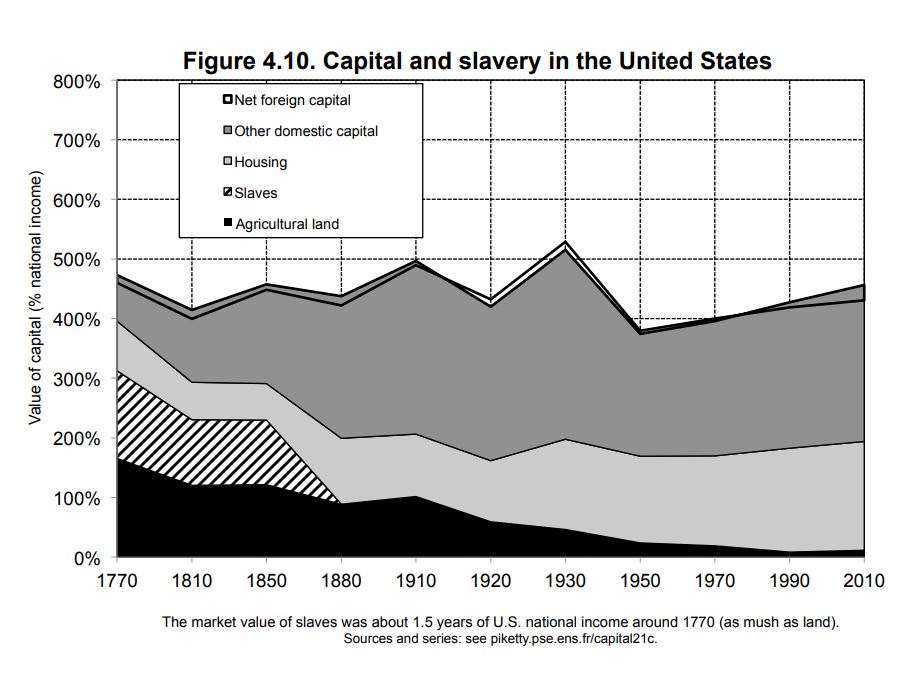

The Dynamics of the Capital/Income Ratio in the United States

In the United States, more than 95% of the assets are American-owned but the influence of landlords and historically accumulated wealth was less important in the U.S. than in Europe. However, the structure of capital in the United States took on a different form. Specifically in the South, slave capital largely supplanted and surpassed landed capital. So much so, that the total market value of slaves represented nearly a year and a half of U.S. national income in the late 18th and first half of the 19th century.

Conclusion

A market economy based on private property, if left to itself, contains power forces of divergence, which are potentially threatening to democratic societies and to the values of social justice on which they are based. My next write-up on Capital in the Twenty-First Century by Thomas Piketty will dive into the immense inequalities of wealth that have occurred as a result of the natural dynamics of capital.

Purpose of this article: to define the emergency fund and help you put together a plan to increase yours.

Bullet Point Summary

Building an emergency fund to cover 3-12 months of expenses will take time

Focus first on saving $1,000 as soon as possible

Commit to saving all windfall payments you receive like tax refunds or any year-end company bonuses

Over the long-term you will need to spend less to save more and look to make more income overall

Building a good budget that helps you cut back on spending will be key

Save any yearly raise received. 1% to 3% can add up quickly

Rinse and repeat until you hit your goal

Overview

Ask any financial planner and they will tell you that an emergency fund is a must. Some will suggest you save upwards of three months of expenses while others will tell you one full year. In this article we discuss the ins and outs of the emergency fund and conclude by giving you strategies to boost your emergency funds.

What Are Emergency Funds For?

The ultimate point of the emergency fund is to set aside cash to cover your most basic needs during an unexpected life event. We all have differing wants and desires in life, but our basic biological requirements for survival are the same. When push comes to shove, we need air to breathe, food and drink, a place to lay our heads at night, and clothes to wear, as depicted in Maslow’s Hierarchy of Needs:

Maslow’s Hierarchy of Needs

Consequently, an emergency fund needs to be established to cover unexpected financial situations like the eviction from an apartment, loss of a job, medical bill, or temporary disability to name a few. In these situations, you’ll need immediate access to cash to cover your most basic expenses and needs while you get your financial situation back on track.

Is There a Right Number?

In a 2018 article, CNBC found that only 39% of Americans had enough savings to cover an $1,000 emergency. Defining the “right number” for an emergency fund is hard because financial emergencies by their very nature are unplanned and their lengths unknown. Instead, we suggest thinking through some of the larger types of unexpected life events that could cause you to dip into your emergency fund and planning specifically for those:

Loss of steady income from primary job – it takes roughly one month per $10,000 you make to find job per thebalancecareers.com. So a person making $50,000 a year would need at least five months of income saved up (roughly $21,000) to tidy themselves during their job hunt.

Car repairs and maintenance – depending on the severity of repair, costs can range from $300 for a water pump replacement up to $3,000 for a transmission replacement.

Major household repairs – similar to car repairs the cost of household repairs will very with the severity of the repair. An new HVAC system can cost 3,800+ while a new roof can run into the tens of thousands.

Using these four large unplanned expense, we build the following table to give you suggested savings targets at differing levels of income:

These savings targets are simply estimates and provide months of coverage ranging from 6 to 12 months. The most important thing is for you to see how expensive unplanned emergencies can be and start actively saving for them.

Short-Term Steps to Build Your Emergency Fund Over Time

It will take time to build a robust emergency fund with three to twelve months of expenses. With competing interests like saving for retirement and paying down debt, it can be difficult to find the extra cash needed to build your emergency fund. The following are the first couple of steps you can take in the short-term that will allow you to build temporary cushion for emergencies.

Your first step will be to save $1,000 as soon as possible. As we mentioned above, only 39% of Americans had enough savings to cover an $1,000 emergency. By focusing here, you are giving yourself a tangible goal that will help give you real cushion against any financial emergencies in the short-term. Set up an automatic transfer from your checking account to an online savings account like Ally of at least 3% of each paycheck. Someone making $40,000 would have over $1,000 in one year:

This assumes that your emergency fund doesn’t accrue any interest which isn’t the case especially if you put your funds in an Ally online savings account. As of the date of this article 5/22/19 Ally’s interest rate on their online savings account was 2.20%.

Your second step will be to save all windfall payments you receive like tax refunds or any year-end company bonuses you may receive. In the past tax refunds had averaged close to $2,100, but this year that was down to about $1,950. Even still, you should put this injection of cash directly into your emergency fund and get one step closer to peace of mind.

These steps are meant to help you build a temporary cushion for emergencies in a short amount of time. Once you complete these steps you will switch your focus to paying down debt if you are not debt-free. And once you are debt-free you will refocus on aggressively building a more robust and complete rainy day fund to cover three to twelve months of expenses.

Long-Term Steps to Build Your Emergency Fund Over Time

It will take time to build a robust emergency fund with three to twelve months of expenses. You should view view building enough emergency savings as a long-term project that will get easier as you free up more cash from the burden of life’s expenses.

Over the long run it will be important that you do two things very well: (1) spend less to save more and (2) make more income. As simple as this may seem, these two factors are the key to building your emergency fund in the long-run.

In order to spend less you will need to build a good budget that helps you cut back on spending. Knowing exactly how much you spend monthly will be key and we suggest using a digital app like Mint or You Need A Budget to track your expenses. The ultimate goal is to bring light to your monthly cash inflows and outflows which will help you free up funds to accelerate the growth in your cash reserves.

Boost your savings by bringing in more income through a side hustle or part-time job even if only temporarily. Make sure to save any yearly raises received. The average pay raise is around 3%, so a person making $40,000 would have an additional $1,200 to save towards the emergency fund over the next year.

Continue to execute the short-term and longer-term strategies discussed above until you hit your goal of three to twelve months of emergency savings.

Conclusion: Remember It Takes Time

An estimated 530,000 families go bankrupt each year because of medical issues, so it’s clear that medical expenses are a big unplanned life event. On top of unplanned medical expenses, there are a ton of other life events that happen unexpectedly that can derail your longer-term financial plans.

The only way to ensure that you will be truly financially secure in times of crisis is to build a robust and well-padded emergency fund. It takes some real time and effort to build a robust enough emergency fund that can handle three to twelve months of expenses, but it’s absolutely doable. We hope the strategies detailed within this article will give you a good enough guide to start building your emergency fund.

Purpose of this article: to explain why you should open an Online Savings Account with Ally Bank today

UPDATE (12/20/19): the current annual percentage yield (APY) for the online savings account with Ally as of December 2019 is 1.60%.

UPDATE (6/20/19): the current annual percentage yield (APY) for the online savings account with Ally as of June 2019 is 2.20%.

Bullet Point Summary

Ally continues to be one of the few financial institutions that consistently gives returns back to its customers.

The APY that Ally offers for its online savings account is one of the best out there.

The Online Savings Account is easy to use, with no maintenance fees, and very few restrictions.

Your deposits are insured by the FDIC up to the maximum allowed by law which is $250,000.

The only thing to watch out for is that you will owe taxes on the interest you receive within this account. Ally will send you a 1099-INT.

Overview

Ally Bank recently announced an increase to their annual percentage yield (APY) which is the interest rate they pay you on your savings deposits with them. Over the past 12 months, they have increased this rate from 1.0% to 1.80% and have one of the highest rates of all banks out there:

With no minimum deposit requirements, and a seamless online experience, everyone should maximize their savings by opening an account with Ally Bank today.

It’s Simple… Your Money Grows More with Ally Bank

Because Ally pays a higher interest rate than most banks, your money grows much faster with Ally. The following graph shows what $1,000 is worth in 30 years across a sample of different banks. Please note that inflation has not been considered and thus the 30-year returns have not been adjusted downwards for simplicities sake:

Before consideration of the impact of inflation, a $1,000 deposit with Ally Bank today would net you $1,708 in 30 years!

Compare to the average of the big banks (PNC, Wells Fargo, and Bank of America to name a few), Ally Bank is a NO BRAINER!!!

Features of the Online Savings Account

*Taken directly from the Ally Bank website. See link here:

• No monthly maintenance fees

• Earn a rate 20x higher than the national average

• Deposit checks remotely with Ally eCheck Deposit

• Grow your money faster with interest compounded daily

• Six transactions limit per statement cycle

• Your deposits are insured by the FDIC up to the maximum allowed by law which is $250,000

• Protect your legacy. Open this account for a Trust. Learn more

Closing

Very rarely are money management decisions this easy. When it comes to maximizing your savings, an Online Savings Account with Ally Bank is simplest and most effective way to go. My hope in writing this article is that after reading this, you will visit Ally Bank and open an Online Savings Account. Your future-self thanks you!