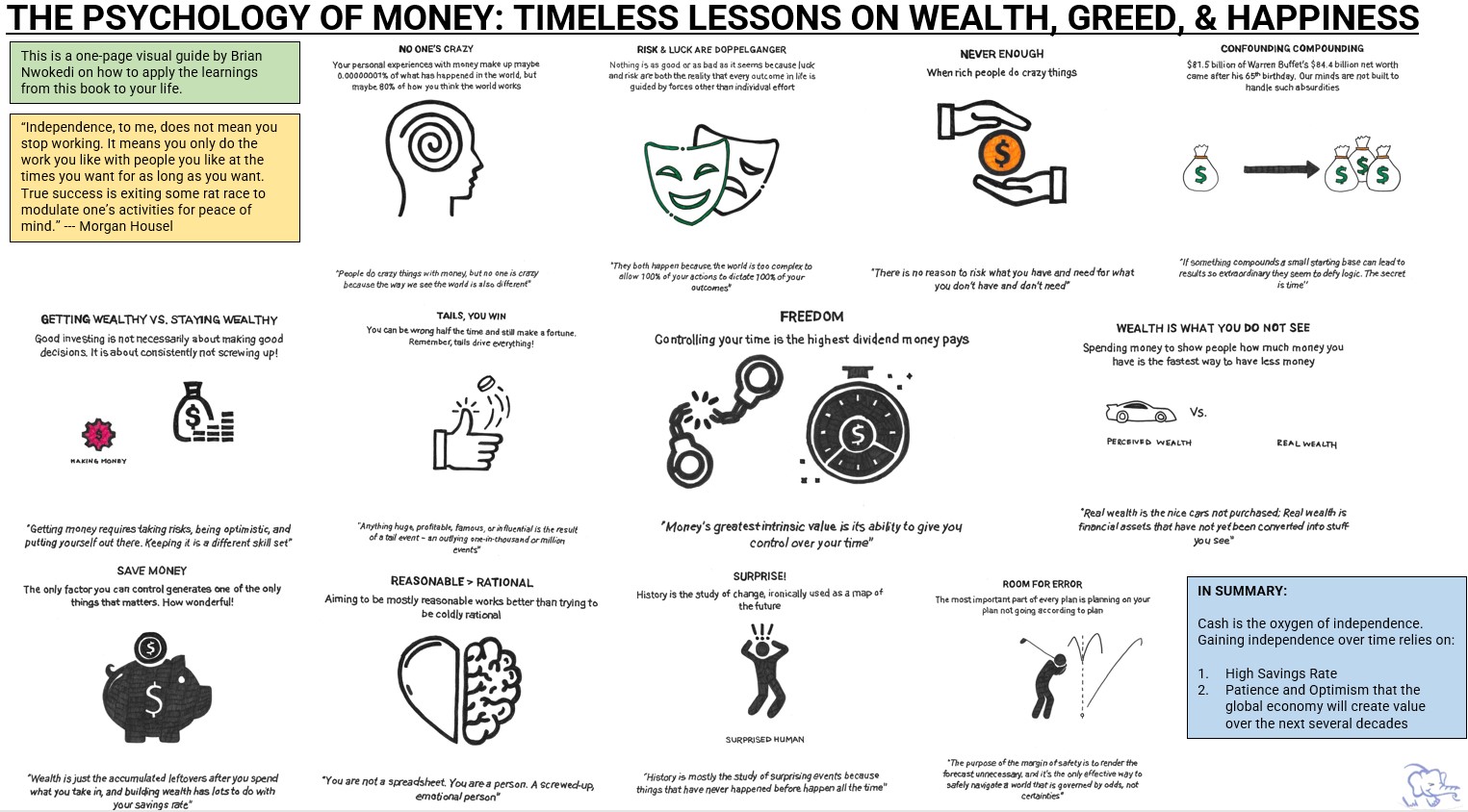

"Success with money relies more on Psychology than Finance,and doing well with money has little to do with how smart you are, and a lot to do with how you behave. And behavior is hard to teach, even to really smart people." --- Morgan Housel (2020)

📚 Core Insight

Success with money is about behavioral discipline, not technical intelligence.

Smart people fail financially because behavior > IQ when it comes to money.

Emotional control, patience, decision-making matter more than financial formulas.

“The Psychology of Money“ by Morgan Housel is an insightful guide that puts the spotlight of financial success squarely on the shoulders of human behavior. In this world of complexity, how you behave with money is more important than what you know about money.

With a blend of research, anecdotes, and stories of personal experiences, Housel illuminates the significance of better understanding your own behavior, and how that is far more responsible for your financial outcomes than your skill.

The following one-page visual guide has been created by me to help you apply the teachings from Morgan’s book to your life. See below ?

Downloadable Content – Raw Notes

Ready to dive deeper into Morgan Housel’s work on The Psychology of Money? Download my unfiltered notes below ?

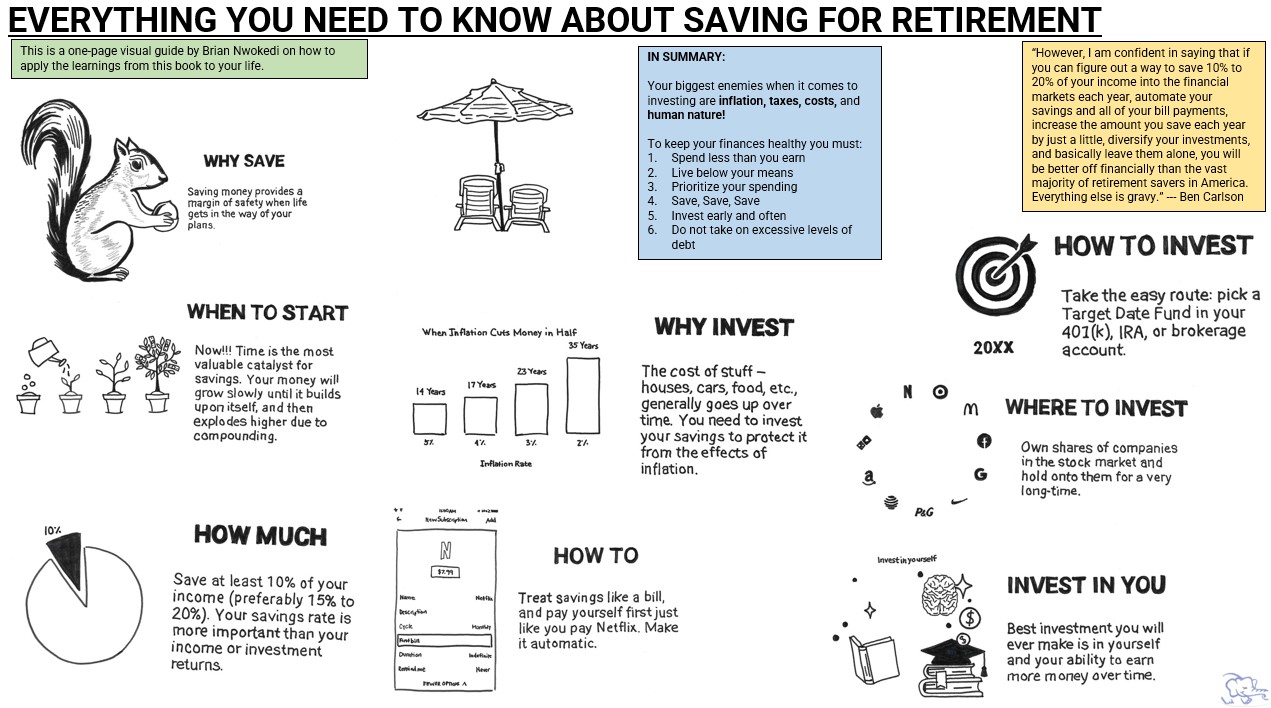

“However, I am confident in saying that if you can figure out a way to save 10% to 20% of your income into the financial markets each year, automate your savings and all of your bill payments, increase the amount you save each year by just a little, diversify your investments, and basically leave them alone, you will be better off financially than the vast majority of retirement savers in America. Everything else is gravy.” --- Ben Carlson(2020)

📚 Core Insight

Building financial independence isn’t about complex investment strategies — it’s about mastering simple behaviors consistently over decades.

The real drivers of retirement success are: saving early and often, automating your habits, resisting lifestyle inflation, and focusing relentlessly on what you can control (your savings rate and behavior) — not chasing high investment returns.

Patience, discipline, and consistency—not brilliance—win the long game.

“Everything You Need to Know About Saving for Retirement“ by Ben Carlson is a succinct yet insightful guide that puts the spotlight on a fundamental aspect of retirement planning: your savings rate. In a world of complex investment strategies and ever-changing financial landscapes, Carlson distills his wisdom into a straightforward message – it’s not just about where you invest, but how much you save.

With a clear and approachable style, he emphasizes that building a secure retirement is within reach if you focus on increasing your savings and maintaining a consistent approach. Drawing on his expertise in personal finance, Carlson’s concise and no-nonsense approach empowers readers to take control of their financial destinies, offering a roadmap to achieving financial security during retirement through a smart savings strategy!

The following one-page visual guide has been created by me to help you apply the teachings from Ben’s book to your life. See below ?

Downloadable Content – Raw Notes

Ready to dive deeper into Ben Carlson’s work on Saving for Retirement? Download my unfiltered notes below ?

Purpose of this article: (1) to show the average retail markup on Green Smoothies and Clean Juices, (2) a solution to save money by making these items at home, and (3) the financial decision making concept of payback period.

Overview

About a year and a half ago I go a NutriBullet PRO, and like most gifts like this, I planned to make the “most out of it”. Unfortunately much like my Latte Habit, I continued to buy store made smoothies from the variety of shops we have here in Charlotte.

Fast forward to 2020, and the resulting shutdown due to COVID-19, and store bought smoothies suddenly became obsolete. Life has a funny way of sometimes making and/or forcing you to appreciate the things you have. And the global pandemic did exactly that for my NutriBullet PRO.

Since pretty much the start of lockdown in March of 2020, my wife and I have adopted a daily Green Smoothie habit; brought to us by none other than the same NutriBullet PRO that originally sat in the kitchen pantry gathering dust. What started as a simple trial has now blossomed into a daily enterprise of good health decisions: (1) a daily green smoothie from our NutriBullet followed by (2) a clean juice from our Aicok Juicer:

The following is my attempt to calculate the financial benefits that have accrued to us as a result of switching to home made green smoothies and clean juice.

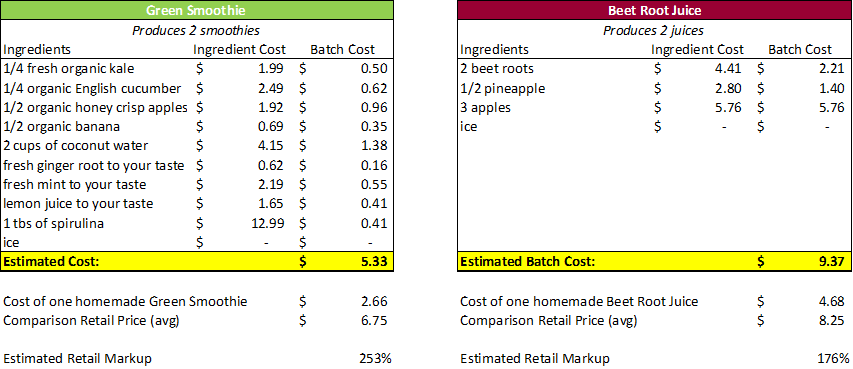

EstimatedCost of a Homemade Green Smoothie & Juice

Our two go-to recipes for green smoothies and clean juice are as follows:

Using the menu of one of my favorite smoothie and juice establishments here in Charlotte I get an average retail price of $6.75 and $8.25 for smoothies and juices respectively. This represents a markup of +176% to $253% on average!!!

Use the Concept of Payback Period to Evaluate

When deciding whether or not to buy a new machine for our house, analyzing the payback period can be an effective financial decision making tool. Most of the time when considering such investments or purchase decisions, the time value of money should be applied to your analysis. This simply means that you should consider the fact that your money today is worth more than that same sum of money in the future due to the fact that your money today can earn interest or a return.

Sometimes though when the investment decision is simple and involves relatively smaller sums of money, analysis of the payback period can be a suitable alternative. The payback period is the amount of time it takes you to recover the initial cost of an investment or purchase. You calculate this by dividing the amount of the original investment by the annual cash flow or net benefit (in the case of my green smoothie/juice machines) derived from the investment.

Using the concept of payback period, lets analyze my Green Smoothie and Juice Machines:

Besides the obvious health benefits of our daily Green Smoothie and Clean Juice habit, the financial implications are immense. After investing in a NutriBullet Pro, it will take roughly 21 days of Green Smoothies to payback the cost of the machine.

By contrast yet still positive, after investing in an Aicok Juicer, it will take roughly 47 days of Clean Juices to payback the cost of the machine.

There is just no denying how value add both machines have been to our lives both from a health standpoint and a financial standpoint. It’s a no brainer given how quickly both machines payback the original cost when compared to purchasing these items at retail stores.

Purpose of this article: to help you quickly create and monitor your personal balance sheet.

Bullet Point Summary

Before you can improve your current financial situation you need to figure out where you are. The personal balance sheet is a great tool to help you accomplish this.

Personal Capital is my favorite personal finance app and piece of software to show net worth. It will speed up the gathering of your financial information, and will give you an awesome snapshot of your net worth every time you log in.

The personal balance sheet gives you a better view of your total finance picture, better than a budget or net cash flow spreadsheet.

Overview

A personal balance sheet provides an overall snapshot of your net worth (or net wealth) at a specific period in time. It is a summary of your assets (what you own), your liabilities (what you owe) and your net worth (assets minus liabilities). The old business adage “what gets measured, gets managed” rings true in your personal finances as well. Without a personal balance sheet, it becomes very challenging to put forth effective short-term and long-term strategies to improve your finances.

Gathering the Necessary Data

Compiling the necessary financial information to create your personal balance sheet can be an arduous manual process especially if you are not using personal finance software like Mint or Personal Capital. So if you do at least one thing after reading this, start using some personal finance software today! Here is a link to reviews on some of the best personal finance software.

There are a ton of reviews comparing all of the ins and outs of each of the different personal finance apps and software, but my favorite by far is Personal Capital. In short, Personal Capital gives you the best view of your Net Worth, and does this quickly, accurately, and in real-time. Additionally, Personal Capital utilizes Yodlee to sync up to your various financial accounts, and thus has fewer reported sync issues.

It’s not a budgeting tool like YNAB or Mint, and it doesn’t help much with daily cash management (i.e. managing expenses, paying bills, alerts on overspend, etc.). It is though an effective aggregator that can help you manage your short-term and long-term views of your net worth.

Create Your Personal Balance Sheet

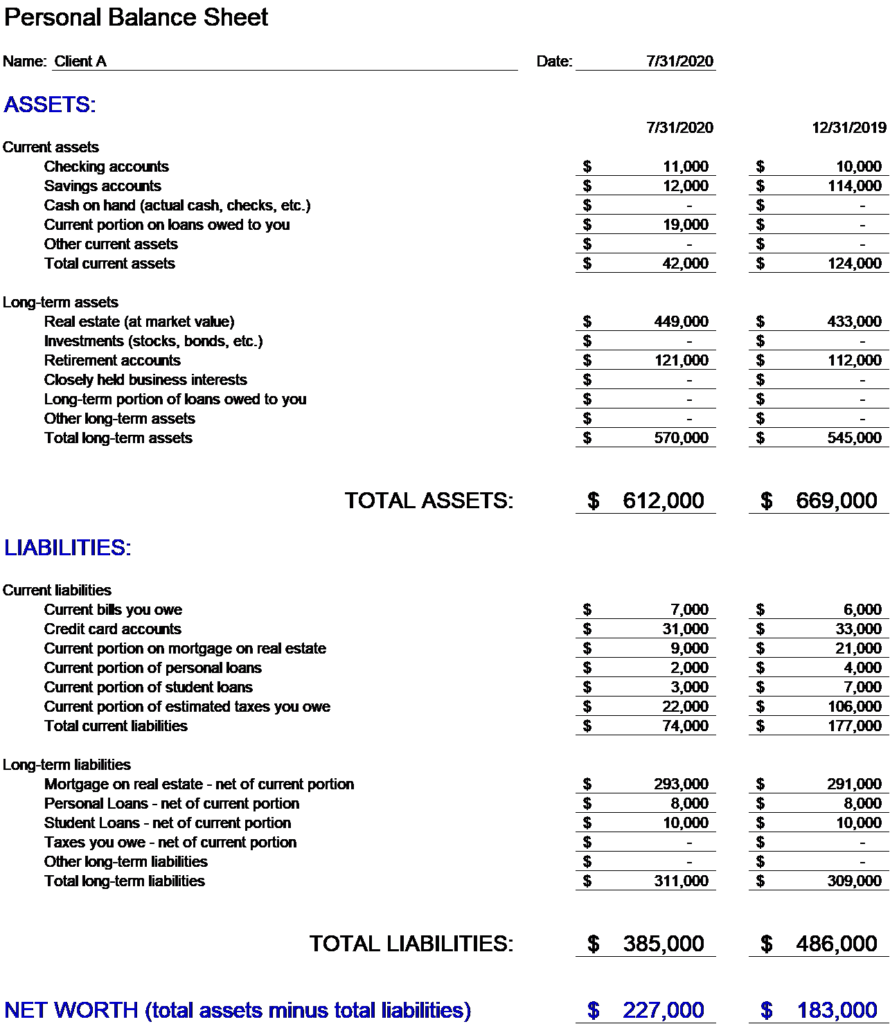

Using Personal Capital, the following personal balance sheet was created for Client A in less than 10 minutes:

All of the values for assets and liabilities are from the same day and thus reflect the same, single point in time for my client’s finances.

What Does It Actually Mean?

Now take a closer look at each column. Over the past seven months there has been a +24% increase in net worth as Client A’s net worth has grown from $183K to $227K. Back in December of 2019, the comprehensive financial strategy that was put in place focused on building retirement assets while steadily paying down liabilities owed, and thus far into the year this strategy is working for Client A.

In general, there isn’t really a magical solution that quickly changes one’s net worth position. Consistently executing your financial plan which usually entails some combination of savings, investing, and paying down debt is the tried and true strategy to increasing your net worth.

But before you can improve your financial situation, you need to measure your current starting point. The personal balance sheet is the best tool to help you do just that, and utilizing the financial app, Personal Capital, makes the compiling and tracking of this information seamless.

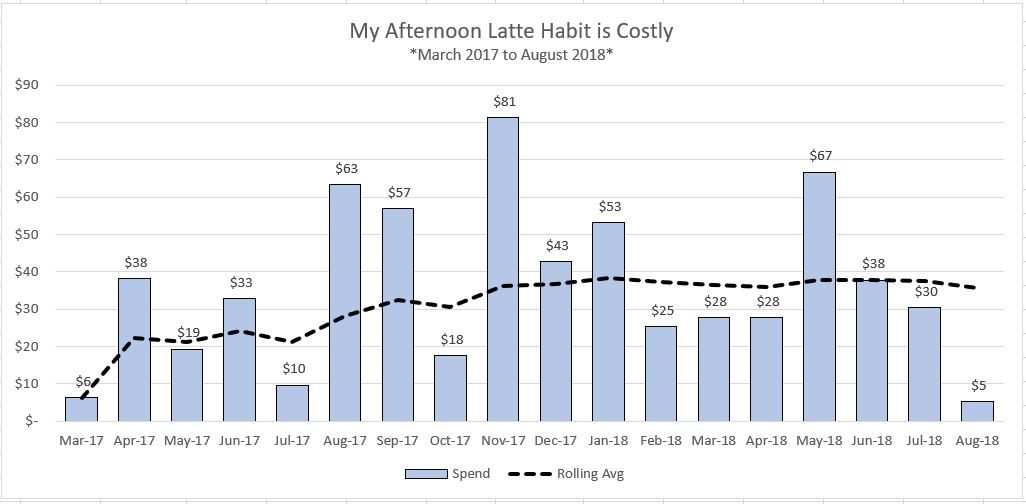

Purpose of this article: to show how my afternoon latte habit adds up and give you some thoughts on things to consider if you have a similar financial habit in your life

Overview

I have a financial confession to make… I love afternoon lattes and it’s costing me dearly! And like many of you out there, I know every single time I buy my latte, I am overpaying severely. According to USA Today’s coffee calculator, the markup on my latte can be as high as 300% depending on the coffee shop. But I will not deny that there is something quite special about a hot off the press latte!

How Much Is My Latte Habit Costing Me?

Based on an analysis of my spending over the last 535 days here are my financial stats:

• I have visited my local Charlotte coffee shops 71 different times, and have spent a total of $643 on afternoon lattes. The cost per trip is $9.04 (my goodness!)

• My average monthly spend over the last 18 months is $35.67

• The most I spent in one month was $81.23 in November 2017

• Over this time period, I spent roughly $1.20 a day on my latte habit.

At a 300% markup, my afternoon latte habit should have only costed $215 if I was disciplined enough to brew my own coffee. This is a difference of $428 extra that I have spent over the last 18 months.

What Could I have Done with the $428?

So, what could I have down with this additional $428? Here are a few things I could have done with that money…

• During the time period of 3/1/17 to 8/18/18 the S&P 500 returned an approximate +19.6%. Had I invested my $428 during this time period, I could be roughly $84 richer.

• Based on the Bureau of Transportation, I could have taken a round trip ticket to almost any US city. The average round trip price during the first three months of 2018 was $346.49.

• I could have used that money to pad my emergency savings account. Recent studies show that very few of us Americans have enough savings to cover a $1,000 emergency.

There are countless other more positive money management actions I could have pursued instead of spending this extra money on my afternoon latte habit. The point I am trying to make here isn’t to pass judgement on this money spending habits. It’s to make myself more aware of an area of spending that may not truly be worth it in the long run.

If you are like me, you probably have some areas of money management that you wish you were better at. I hope my financial habit confession was helpful for you to hear. Please let us know what financial habits you have and wish to break.